Fintech has become an integral part of everyday life as more consumers and businesses turn to digital financial tools for help with spending, saving, budgeting, and investing. To speak to the evolving landscape for fintech leaders, the Financial Technology Association held a “State of Fintech” webinar to unveil insights from Plaid and The Harris Poll on the benefits of digital financial tools and unpack what the data means with fintech leaders Betterment, Cash App, and Intuit.

The Harris Poll’s Fintech Effect Report is an annual consumer survey examining how people use fintech and its impact on managing their financial lives. The report focuses on year-over-year trends, new learnings on the state of fintech, and consumer use in the current economic climate and post-pandemic environment. It includes spotlights on payments, trust and safety, and evolving consumer expectations.

The State of Fintech webinar reinforced that fintech is here to stay and provides value to consumers and small businesses. As consumer expectations evolve around trust, safety, and control, personal financial data rights are paramount to the future of finance. Catch up with four key takeaways on the State of Fintech. Did you miss FTA’s live webinar? Watch the recording here.

#1 Fintech is the new normal

Eight in ten Americans (80%) used digital apps and services to manage their money in 2022, and over half used fintech daily. The average consumer uses three fintech apps, with payments, bill pay, tax filing, online banking, investing, budgeting, and lending emerging as the top use cases. For the first time, fintech adoption rates have equalized across demographic groups and income levels. Among racial groups, Black people (88%) and Hispanic people (92%) continue to use fintech at the highest rates, compared to White people (74%) and Asian people (79%).

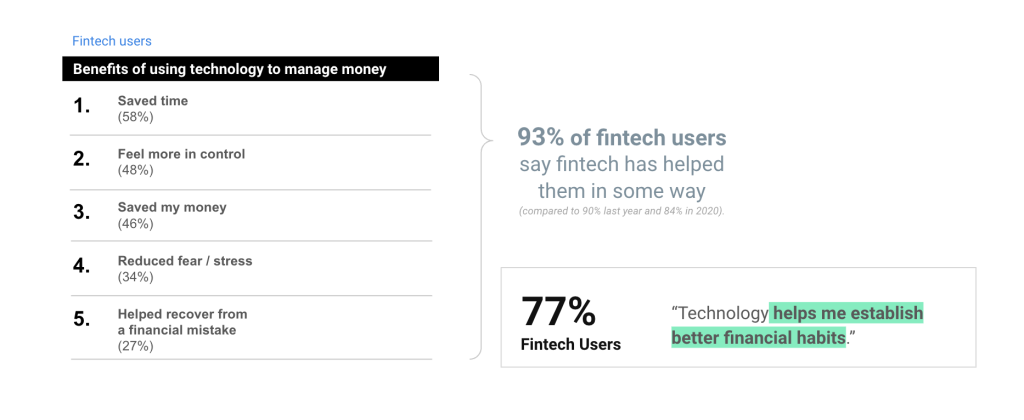

#2 Consumers find value in fintech tools

More than nine in ten users (93%) benefit from fintech tools, and 61% of Americans rely on apps like budgeting tools to weather economic changes. Real-time access to their money remains a top priority for consumers, especially for managing day-to-day costs.

“The most important customer benefit Intuit and other fintech companies can deliver is access,” said Sarah Paul, Director of Global Policy and Regulatory Affairs at Intuit. “Access to expertise, tools, and resources that give people the power to manage their money with confidence. Fintechs are democratizing financial services that are usually only available to a few people, putting technology on the side of consumers and small businesses to solve their biggest problems.”

Payment apps are the top use case for fintech adopters, with consumers turning to them to weather short-term needs and to make ends meet. For example, platforms like Cash App give consumers an easy way to store, send, receive, spend, and invest their money.

“Our platform provides a variety of personal finance tools, including peer-to-peer payments, direct deposit, investing in the traditional stock market and bitcoin, and helping Americans prepare their taxes for free,” said Amena Ross, Head of Policy at Cash App. “We just launched Cash App savings last week, which gives customers tools to automate their savings over time.”

Fintech apps also make long-term planning more accessible, with more than half of consumers starting to invest for the first time with a digital app (53%). ”Digital apps expand access because they are easy to use on any device,” said Raoul Bhavnani, Chief Communications Officer at Betterment, the leading independent digital investment advisor in the United States. “They are available 24 hours a day, 365 days a year. Importantly, they can be constantly updated with the latest security tools, educational resources, content, and suggestions to help make an individual’s investing journey delightful and informative.”

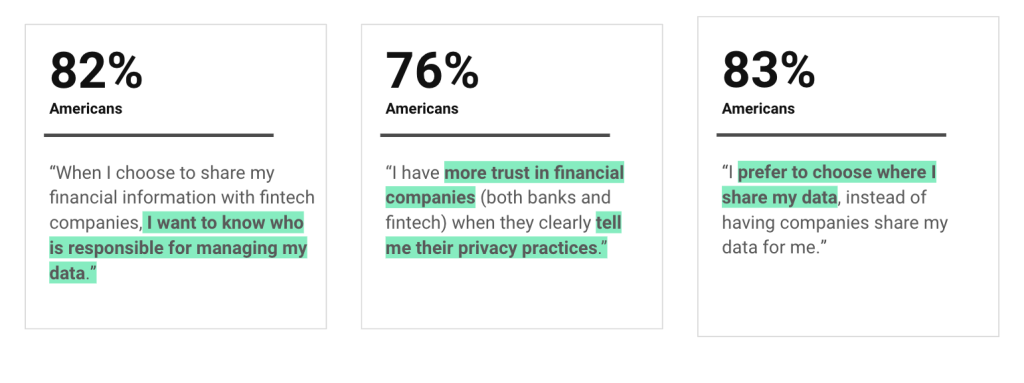

#3 Trust, transparency, and control are paramount to consumers

Consumers increasingly expect trustworthy and secure experiences and want to control who has access to their financial data and how it is used. Fintechs outpace traditional banks on privacy consumers’ expectations, as 61% of American consumers agree that when using fintech applications, they have more control over their financial information than banks.

#4 Personal financial data rights are the future of finance

As consumer expectations evolve, the policies and regulations governing financial services must keep pace. The Consumer Financial Protection Bureau’s rulemaking to implement section 1033 of the Dodd-Frank Act and establish personal financial data rights is an excellent example of empowering consumers to securely control, access, and share their financial data. Fintech leaders agree that 1033 is critical to unlocking competition and consumer choice.

“Without a 1033 rule in place, our customers would have varying experiences and different benefits depending on how their bank manages their permissioned access by third parties, reiterated Sarah Paul of Intuit. “We fully support a 1033 rule that gives consumers and small businesses access and control over their financial information. This allows them to easily use third-party financial products that best meet their needs and circumstances.”

The 1033 rule should include security and privacy assurances that third parties will protect consumer information and only use it for stated purposes, giving consumers clear insight into how their data is used. Expanding the 1033 rule beyond just bank account data to encompass accounts like mortgages, investments, and student loans would empower consumers with a complete picture of their financial lives and more control of their personal financial information.